Home Care vs. Facility Care

Home Care vs. Facility Care

Home care is the overwhelmingly preferred setting for most people who contemplate needing long-term care. That preference is understandable and legitimate. But "staying home" is not a single, fixed option — it is a spectrum of arrangements that grows in cost and complexity as care needs intensify. At lower levels of need, home care is often cheaper and appropriate. At higher levels of need, 24-hour home care can exceed the cost of nursing home care in many markets while providing fewer safety safeguards. This page explains how home and facility care compare across key dimensions, what typically triggers a transition, and where the cost crossover points occur.

Understanding the Setting Spectrum

Long-term care is not a binary choice between "home" and "nursing home." The care setting spectrum includes:

-

Home care with periodic aide support (part-time personal care, homemaker services)

-

Home care with skilled nursing visits (wound care, medication management, therapy)

-

Adult day programs (structured daytime programming in a group setting; individual returns home in evenings)

-

Assisted living (residential care with personal care services; not skilled nursing)

-

Memory care (specialized assisted living for dementia; secured environment, cognitive programming)

-

Skilled nursing facility (nursing home; highest level of residential care with 24-hour nursing)

-

Continuing care retirement community (CCRC) (campus offering multiple levels, often under one contract)

Each setting on this spectrum addresses a different level of care need, offers different services, costs differently, and is covered differently by Medicare, Medicaid, and LTC insurance. The appropriate setting for any individual depends on the nature of their functional limitations, their safety needs, the availability of family support, and financial resources.

Why the Choice Is Not Static

A person's appropriate care setting at the onset of a care need is often different from the appropriate setting two or three years later. Dementia progression, physical decline, falls, and medical complexity frequently require transitions from lower-intensity to higher-intensity settings. Planning for only the first setting and not the likely trajectory understates the full scope of what long-term care will require.

Home Care vs. Facility Care: Key Dimensions

The following table compares home care and facility care across ten key dimensions. Both settings have meaningful strengths and meaningful limitations.

Three observations from the table deserve emphasis:

-

Overnight and weekend coverage is the most common gap in home care. Aide services typically run 8-hour shifts. When a person needs care at 2 AM or on a Sunday, the aide may not be present. Facility care provides 24-hour staff as a baseline.

-

Family caregiver burden is often higher with home care, not lower. Home care is frequently described as relieving family of caregiving responsibility — but the family often coordinates care, fills shift gaps, handles medical appointments, and manages crises. The role changes from hands-on care to logistics-and-oversight, which carries its own significant burden.

-

Isolation is an underestimated home care risk. Without structured social programming, a person receiving home care may have limited peer interaction, particularly if they are no longer driving. Social isolation is associated with cognitive decline, depression, and reduced quality of life in older adults.

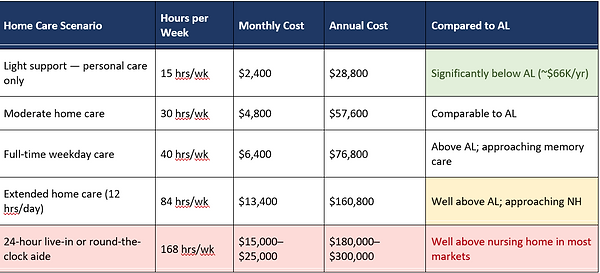

The Cost Crossover Point

One of the most counterintuitive aspects of long-term care planning is that home care is not always cheaper than facility care. The comparison depends almost entirely on how many hours of aide coverage are needed.

The cost crossover point — where home care becomes more expensive than assisted living or nursing home care — is not a theoretical edge case. It is the likely outcome for anyone whose care needs require more than approximately 35–40 hours of aide coverage per week. Advanced dementia, severe mobility impairment, and complex medical needs can push care requirements well into the 24-hour range, at which point professional home care in most markets costs more than residential facility care — while also providing fewer supervision and emergency response capabilities.

The "I'll Just Hire Help" Assumption

Many households underestimate the cost of home care because they think of it as periodic help rather than full coverage. The assumption is often: "We'll hire someone for a few hours a day." But a progressive condition like Parkinson's disease or Alzheimer's does not remain at "a few hours a day" indefinitely. The relevant financial question is not what home care costs at the beginning of a care need — it is what it costs at the midpoint and end, when needs are most intensive.

What Typically Triggers a Transition to Facility Care

Most transitions from home to facility care are not planned events — they are responses to a specific incident or an accumulation of incidents that make continued home care unsafe or unsustainable. The following table identifies the most common triggers and the typical family response.

The most important pattern in the table: the triggers that force facility transitions are clinical and safety events, not financial decisions. Families often want to keep a loved one at home as long as possible — and frequently do — but safety incidents (falls, wandering, medication errors, acute hospitalization) are what ultimately determine when home care is no longer adequate. Planning that accounts for this transition — rather than assuming it will not occur — reduces the crisis response when it does.

The Family Caregiver Variable

Any comparison of home care and facility care must account for the family caregiver dimension. Home care in practice is rarely provided solely by professional aides — it typically involves a combination of paid aide coverage and unpaid family caregiving. The distinction matters financially and personally.

Unpaid family caregiving has a documented economic cost — studies estimate an average of 20+ hours per week for family caregivers of adults with significant care needs. This labor has value that does not appear in care cost comparisons but is real in terms of family members' time, career impact, and health. When home care appears cheaper than facility care, part of that "savings" reflects cost transferred to unpaid family labor.

The Caregiver Health Risk

Research consistently shows that informal caregivers — predominantly spouses and adult daughters — face elevated rates of depression, anxiety, and physical health decline compared to non-caregivers. Caregiver burnout is not just a quality-of-life issue; it is a health risk that can result in the caregiver themselves needing care. A home care plan that relies heavily on a single family caregiver without respite or backup coverage is structurally fragile.

This does not mean facility care is always preferable — many families provide extraordinary care at home for years, and many care recipients thrive in familiar environments with family involvement. It means that the family caregiver's capacity, health, and other obligations are a real variable in any home care plan, and that plan should include what happens when that variable changes.

Insurance Coverage Across Settings

How care is funded differs significantly by setting:

-

Medicare covers short-term skilled nursing in a facility (up to 100 days after a qualifying hospital stay) and limited home health services, but does not cover custodial care — the ongoing personal care that constitutes most long-term care need — in any setting.

-

Medicaid covers nursing home care (subject to eligibility) in all states. Home and community-based services (HCBS) are covered through state waiver programs, but slots are limited and waitlists in many states are 1–5 years long.

-

Traditional LTC insurance typically covers home care, adult day, assisted living, memory care, and nursing home care — but with an elimination period (typically 90 days of qualifying care costs) before benefits begin. Some policies pay a lower benefit for home care than for facility care.

-

Hybrid LTC products generally follow similar coverage structures but with benefit acceleration triggered by the same ADL/cognitive impairment criteria.

One practical implication: a person who wants to remain at home long-term and has LTC insurance should confirm that their policy's home care benefit — daily benefit amount, covered services, and inflation protection — is sufficient to cover likely aide costs in their market. In high-cost urban areas, a policy with a $150/day benefit may cover only a few hours of daily home care.

Trade-Off Summary

Home care preserves familiarity, autonomy, and connection to a person's own environment. At lower levels of need and with adequate family support, it is often the most appropriate and cost-effective option. As care needs intensify — more hours of aide coverage, overnight supervision, safety monitoring, medical complexity — home care becomes progressively more expensive, more logistically complex, and more dependent on family caregiver capacity that may not be sustainable.

Facility care is not the failure scenario it is sometimes portrayed to be. Well-chosen facilities provide 24-hour safety monitoring, social engagement, medical coordination, and relief for family caregivers. The appropriate setting depends on the stage and nature of a person's care needs — and both settings serve important roles across a long-term care trajectory.

Summary

Home care and facility care are not competing choices so much as sequential phases for many people. Home care is appropriate and often preferred at lower levels of need. At high levels of need — particularly 24-hour supervision requirements — home care typically costs more than residential facility care while providing fewer safety safeguards. Transition triggers are usually clinical (falls, wandering, hospitalization), not financial, and most are not planned in advance.

The family caregiver variable is frequently underweighted in home care plans. Unpaid family labor has real economic and health costs that do not appear in cost comparisons but are real. A complete long-term care plan addresses both the paid care costs and the sustainability of family involvement across a likely multi-year care trajectory.

Frequently Asked Questions

Q: Is home care always preferred over facility care?

Home is the preferred setting for most people — surveys consistently show strong preference for aging in place. But preference and clinical appropriateness are different questions. At higher levels of need, home care may be less safe, more expensive, and more burdensome to family than a residential facility. Preference matters; it should be balanced against what the care need actually requires.

Q: At what point does home care become more expensive than a nursing home?

The crossover point varies by market and aide wages. As a rough benchmark: when aide coverage exceeds approximately 35–40 hours per week at 2025 national median rates ($32–$35/hr), monthly costs approach assisted living range ($5,000–$6,000/mo). When 24-hour coverage is required ($15,000–$25,000/mo), home care substantially exceeds nursing home costs in most markets. In high-cost urban markets (New York City, San Francisco), the crossover happens earlier.

Q: Does Medicare cover home care?

Medicare covers limited skilled home health services — nursing, physical therapy, occupational therapy — when the person is homebound and the services are medically necessary. Medicare does not cover custodial care: assistance with bathing, dressing, toileting, meal preparation, or supervision. Custodial care is the majority of what long-term care need consists of. Medicare's home health coverage is time-limited and applies only to skilled, physician-ordered services.

Q: Can Medicaid pay for home care?

Medicaid's Home and Community-Based Services (HCBS) waivers can cover home care for Medicaid-eligible individuals. However, HCBS waivers are optional state programs with limited slots. In many states, the waitlist for HCBS services is 1–5 years. Medicaid will cover nursing home care without a waitlist for eligible individuals; it will not always cover home care on the same timeline. This asymmetry means Medicaid may provide a path to nursing home coverage sooner than to home care coverage for a low-income person who needs care now.

Q: What is adult day care and how does it compare to other options?

Adult day programs provide structured daytime programming — social activities, meals, health monitoring, and sometimes therapy — in a group setting outside the home. The person returns home in the evening. Adult day programs can reduce caregiver burden, provide social engagement for the care recipient, and supplement or reduce the need for home aide hours. Costs are typically $80–$120 per day, making full-time adult day programs ($1,600–$2,400/month) significantly less expensive than full-time home aide coverage.

Q: What should families look for when evaluating a care facility?

This page does not provide facility evaluation criteria, as that is a clinical and operational question that goes beyond financial planning. General reference points include: state inspection reports (available through Medicaid's Nursing Home Compare tool), staff-to-resident ratios, staff turnover rates, programming for the specific condition (e.g., dementia programming in memory care), physical environment quality, and feedback from current residents and families. The appropriate evaluation depends on the type of facility and the care need.

Q: How does a person's LTC insurance policy treat home care vs. facility care?

LTC insurance policies vary. Some pay the same daily benefit regardless of setting; others pay a lower benefit for home care than for facility care (e.g., 50% or 75% of the facility daily benefit). Some policies have separate benefit pools for home and facility care; others use a shared pool. The elimination period may apply differently by setting on older policies. A policyholder planning to rely on home care should review the policy's home care benefit specifically, not just the overall benefit amount.

Q: Does moving to a facility mean giving up control?

Facility residents retain legal rights — including the right to participate in care planning, refuse treatment, and receive visitors. Federal law (the Nursing Home Reform Act) establishes a Residents' Bill of Rights for skilled nursing facility residents. That said, facility care involves less autonomy over daily schedule, environment, and routine than living at home. The degree to which this matters depends on individual values and the specific facility's culture and practices.

Q: Can a person move between home care and a facility based on changing needs?

Yes, and for many people this is the realistic trajectory. A person may receive home care in the early phase of a progressive condition, transition to assisted living as needs increase, and later move to memory care or skilled nursing as the condition advances. LTC insurance policies generally cover all qualified settings from the same benefit pool, so a transition between settings does not reset the elimination period or reduce the available benefit (though the daily draw may increase).

This page does not recommend whether any individual should receive care at home or in a facility. That determination depends on clinical needs, safety, family capacity, and individual values that this reference page cannot assess.

This page does not assess the quality of specific home care agencies or facilities. Quality varies significantly within each category; evaluation requires direct due diligence.

Cost figures are national medians for 2025. Regional variation is substantial — urban coastal markets are typically 20–50% higher. Costs should be verified locally.

For informational use only. Not legal, tax, or financial advice.