Hybrid Life/LTC Products — How They Work

What are hybrid life/LTC products, how do they differ from standalone LTC insurance, and what trade-offs do they involve?

Why Hybrid Products Emerged

The most common objection to standalone long-term care insurance has always been the same: "What if I pay premiums for 30 years and never need care? I've wasted all that money." This "use it or lose it" concern prevents many households from purchasing LTC coverage despite recognizing the underlying risk.

Hybrid life/LTC products were developed specifically to address this objection. By linking LTC benefits to a life insurance policy or annuity, the product ensures that premium dollars are not forfeited if care is not needed — either LTC benefits are paid during life, or the death benefit is paid at death. The premium is "used" either way.

The growth of the hybrid market accelerated significantly as standalone LTC carriers exited the market in the 2010s. By the mid-2020s, hybrid products represent the majority of new LTC-related product sales by premium volume. Understanding how they work — and where they differ from standalone LTC — is essential context for evaluating any LTC funding strategy.

The Product Types

The hybrid category includes several distinct product structures. Each uses a different base insurance vehicle and structures the LTC benefit differently.

Single-Premium Products: Repositioning Idle Assets

Single-premium hybrid products are frequently used to reposition assets that are currently sitting in low-yield vehicles — CDs, money market accounts, short-term bonds. A $100,000 CD earning 4% can be repositioned into a single-premium life/LTC product that immediately creates a $200,000–$300,000 LTC benefit pool and a comparable death benefit. The insured gives up the CD's liquidity (subject to surrender charges) in exchange for the LTC and death benefit leverage. This repositioning is most appropriate for assets genuinely earmarked as a reserve rather than needed for near-term liquidity.

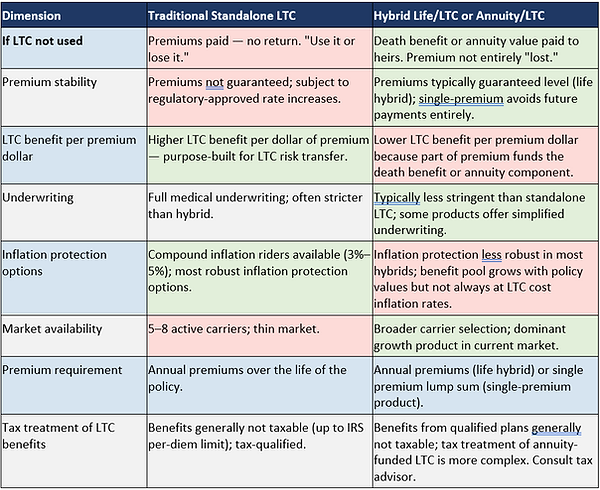

Hybrid vs. Standalone LTC: A Direct Comparison

The Core Trade-Off in One Statement

Standalone LTC insurance provides more LTC coverage per dollar of premium — but premium dollars are forfeited if care is not needed and premiums can increase. Hybrid products guarantee no waste and stable premiums — but provide less LTC benefit per premium dollar and weaker inflation protection. Neither is universally better. The right choice depends on the household's priorities, asset position, and LTC risk profile.

How Benefits Are Drawn: Acceleration and Extension

In a life-based hybrid, LTC benefits are paid through "accelerated death benefit" provisions — the insured draws down the death benefit tax-free to pay for qualifying LTC costs. Each dollar of LTC benefit paid reduces the remaining death benefit by one dollar.

Example: A policy with a $300,000 death benefit begins an LTC claim. At $6,000/month in benefits, the policy pays for 50 months (just over 4 years) before the death benefit is exhausted. At that point — without an extension rider — LTC benefits end.

An extension-of-benefits rider continues paying LTC benefits beyond the point where the death benefit is exhausted, for an additional defined period (typically 2–5 years). This rider materially improves coverage for long-duration care episodes but increases the product's premium cost.

The Inflation Problem

One meaningful limitation of hybrid products — particularly for policies purchased well before a likely claim — is the handling of LTC cost inflation. Standalone LTC insurance offers compound inflation riders (typically 3%–5% annually) that grow the benefit explicitly in line with LTC cost assumptions. Most hybrid products do not offer equivalent inflation protection.

The benefit pool in a hybrid product may grow through policy crediting rates (for universal life or indexed products) or accumulation rates (for annuities). This growth provides some protection against inflation but is driven by investment performance rather than a defined LTC-specific inflation adjustment. Over a 20–30 year horizon between purchase and claim, the gap between hybrid benefit growth and actual LTC cost inflation can be significant.

For younger buyers (ages 45–55) with a long time horizon, this inflation limitation deserves careful evaluation. For buyers closer to a potential care need (ages 65–75), where the time horizon is shorter, the gap may be less consequential.

Trade-Off Summary: Hybrid Product Advantages and Limitations

-

Use it or lose it

-

Eliminates the principal objection to standalone LTC insurance — premium dollars are not "wasted" if LTC is not needed; death benefit remains.

-

The death benefit component means some of every premium dollar funds life insurance rather than LTC risk transfer — reducing pure LTC leverage.

-

-

Premium certainty

-

Guaranteed or level premiums eliminate the risk of regulatory-approved rate increases that have hit standalone LTC policyholders hard.

-

The initial premium is typically higher than comparable standalone LTC coverage. Single-premium products require a large upfront capital commitment.

-

-

LTC benefit size

-

For households primarily concerned with asset preservation rather than maximum LTC benefit, the combined death benefit + LTC pool may be sufficient.

-

Per dollar of premium, hybrid products typically provide less LTC benefit than standalone LTC. Households needing very large LTC benefit amounts may find hybrids insufficient.

-

-

Inflation coverage

-

Policy value growth (in indexed or universal life products) provides some inflation hedge.

-

Compound LTC-specific inflation protection is less robust in most hybrid products than in standalone LTC. Long purchasing timelines magnify this gap.

-

-

Capital efficiency

-

Single-premium products allow repositioning of low-yield assets (CDs, savings accounts) into a vehicle with LTC and death benefit components.

-

The capital committed to a single-premium product is illiquid. Surrender charges apply if the policy is terminated early.

-

-

Underwriting access

-

Less stringent underwriting in many hybrid products allows people who would be declined for standalone LTC to obtain some coverage.

-

Simplified underwriting typically results in higher premiums or reduced benefit multiples relative to fully underwritten products.

-

Tax Considerations

The tax treatment of hybrid products involves several considerations:

-

Life insurance death benefits: Generally paid income-tax-free to beneficiaries.

-

LTC benefits from life-based hybrids: Benefits drawn from the death benefit for qualifying LTC costs are generally not taxable income, up to the IRS per-diem limit ($420/day in 2026). Benefits above this limit may be taxable.

-

Annuity-based LTC: The tax treatment is more complex. Annuity gains are taxed as ordinary income when withdrawn. However, LTC benefits from a qualified (tax-qualified) plan are generally not taxable. The interaction between annuity taxation and LTC benefit taxation should be reviewed with a tax advisor.

-

1035 exchange: Existing life insurance or annuity policies can be exchanged for a hybrid product using a tax-free 1035 exchange, allowing repositioning without triggering immediate gain recognition. This is a common funding mechanism for hybrid product purchases.

Summary

Hybrid life/LTC products combine a permanent life insurance policy or annuity with a long-term care benefit. When LTC is needed, benefits are drawn from the death benefit or accumulation value. When LTC is not needed, the death benefit or annuity value passes to beneficiaries. The "use it or lose it" objection to standalone LTC insurance is eliminated.

The trade-offs are real: hybrid products provide less LTC benefit per premium dollar than standalone LTC insurance, offer weaker inflation protection, and require a larger initial premium commitment (particularly single-premium products). They gain in premium stability (level or single premium) and broader market availability as standalone LTC carrier options have declined.

For households primarily concerned about leaving a legacy or repositioning low-yield assets, hybrid products offer an appealing structure. For households prioritizing maximum LTC benefit coverage — particularly for long-duration care scenarios — standalone LTC or a combined approach may provide better LTC leverage per dollar. The appropriate choice depends on individual circumstances, asset position, health status, and planning priorities.

Frequently Asked Questions

What is a hybrid life/LTC insurance product?

A hybrid life/LTC product combines a permanent life insurance policy with a long-term care benefit. The life insurance death benefit serves as the LTC benefit pool — when the insured qualifies for LTC benefits (meets a benefit trigger), they can draw against the death benefit tax-free to pay for qualifying care. If LTC benefits are not fully used, the remaining death benefit is paid to beneficiaries at death. The "hybrid" name reflects the combination of life insurance and LTC coverage in a single product.

What is the main advantage of a hybrid product over standalone LTC insurance?

The primary advantage is the elimination of the "use it or lose it" problem associated with standalone LTC insurance. With traditional LTC, premiums paid over decades generate no benefit if the insured never qualifies for a claim. With a hybrid product, the premium dollars are anchored in a life insurance or annuity value that is paid to someone — either as LTC benefits during life or as a death benefit at death. The premium is not forfeited if care is not needed.

How does a single-premium life/LTC product work?

A single-premium hybrid product is funded with a one-time lump sum deposit — often $50,000 to $250,000 or more — rather than ongoing annual premiums. That deposit immediately creates a death benefit (typically 2x–3x or more the deposit amount) and an LTC benefit pool (typically even larger, depending on product structure). No further premium payments are required. These products are often used to reposition low-yield liquid assets — CDs, savings accounts, fixed annuities — into a vehicle with LTC protection and a death benefit.

How is an annuity-based LTC product different from a life-based hybrid?

An annuity-based LTC product uses a fixed or indexed deferred annuity as the underlying vehicle. The LTC benefit is drawn from the annuity's accumulation value — sometimes multiplied (e.g., 2x or 3x the annuity value) for LTC purposes. If LTC is not needed, the annuity value (plus growth) is available as retirement income or can be passed to heirs. The primary distinction from life-based hybrids is the absence of a life insurance component and the different tax treatment — annuity withdrawals are subject to ordinary income tax rules, though LTC benefits from qualified plans are generally not taxable.

Does a hybrid product provide enough LTC coverage?

This depends entirely on the product design, the premium or deposit amount, and the expected care costs in the relevant location. Hybrid products typically provide less LTC benefit per premium dollar than standalone LTC insurance because part of the premium funds the death benefit or annuity component. For households primarily concerned with protecting assets against a moderate care need, hybrids may be sufficient. For households wanting maximum LTC benefit coverage — especially for long-duration care scenarios — standalone LTC may provide better coverage per dollar of premium.

Can premiums on hybrid products increase?

For most hybrid life products, premiums are guaranteed level — one of the product's primary advantages over standalone LTC. Single-premium products have no future premiums at all. Some universal life-based hybrids have a level premium guarantee period that should be confirmed. Annuity-based products have no ongoing premium; the initial deposit is the full cost. The premium stability guarantee is a core feature of hybrid products that distinguishes them from standalone LTC.

What happens to a hybrid policy if the insured dies before needing LTC?

If the insured dies without having used LTC benefits, the remaining death benefit is paid to the named beneficiaries — typically income-tax-free for life insurance-based products. For annuity-based products, the accumulated value is paid to beneficiaries, subject to the annuity's tax treatment. This is the "no waste" feature: the premium or deposit is not forfeited even if LTC is not needed.

Is a hybrid product right for someone who already has standalone LTC insurance?

An existing standalone LTC policy and a hybrid product serve the same underlying need — LTC risk transfer. Adding a hybrid does not automatically improve a planning situation that may already be addressed. Situations where this question arises include: (a) an existing LTC policy with premium increases that are creating affordability pressure, and the policyholder is considering replacing it; (b) a gap in coverage that the existing policy does not address; or (c) desire for additional protection beyond the existing policy's benefit limits. These decisions involve individual policy analysis and financial planning that is specific to each situation.

What is an extension-of-benefits rider on a life hybrid?

An extension-of-benefits rider adds LTC coverage beyond the base death benefit. Without this rider, LTC benefits are limited to the total death benefit — once the death benefit is exhausted, LTC coverage ends. An extension rider continues paying LTC benefits for an additional defined period (typically 2–5 more years) after the base death benefit is depleted. This rider significantly increases the product's usefulness for long-duration care episodes but adds to the premium cost.

How do hybrid products handle inflation in LTC costs?

Hybrid products handle inflation differently than standalone LTC policies. Life-based hybrids with a growing cash value provide some inflation protection as the death benefit and LTC benefit pool grows with the policy's performance. However, this growth may not keep pace with LTC cost inflation specifically. Indexed products linked to a market index may grow faster but are not guaranteed. Compound inflation riders (like those available on standalone LTC) are less common and generally less robust in hybrid products. This is a meaningful limitation for policies purchased many years before a likely claim.

This page explains how hybrid life/LTC and annuity/LTC products work as a category. It does not: evaluate specific products or carriers; provide premium or benefit illustrations; recommend hybrid products as appropriate for any individual; or substitute for consultation with a licensed insurance professional and financial advisor. Product design varies significantly among carriers and product lines. Tax treatment is complex and depends on individual circumstances. For informational purposes only. Not investment, legal, or tax advice.