What Medicaid Is and How It Functions as a Long-Term Care Payer

Why Medicaid is not Medicare — and what it actually requires before it pays for care

Medicaid and Medicare are frequently confused — not only by the general public but by people actively planning for retirement. They share a similar name, both involve the federal government, and both pay for healthcare in some form. Beyond that, they are structurally different programs serving different populations through different mechanisms.

The confusion matters because Medicaid is the primary payer for long-term custodial care in the United States — covering approximately 62% of nursing home residents nationally. For most Americans, Medicaid is the financial system that actually funds extended care when other resources are exhausted. Understanding what it is, how it qualifies people, and what it does and does not cover is essential context for any long-term care conversation.

This page explains what Medicaid is as a program, how it differs from Medicare, what the qualification requirements are, what it covers and excludes, and the trade-off between treating Medicaid as an unplanned safety net versus as a deliberate planning element.

What Medicaid Is — and What It Is Not

THE FOUNDATIONAL DISTINCTION

Medicare is an earned federal benefit — funded by payroll taxes, available to nearly all Americans at 65 regardless of income or assets. Medicaid is means-tested public assistance — funded by federal and state revenues, available only to people whose assets and income fall below defined thresholds. They are different programs with different eligibility structures and different purposes.

Medicaid was created in 1965 alongside Medicare as the program to provide healthcare coverage to low-income individuals and families. Over time, it became the primary public funding mechanism for long-term custodial care — not because it was designed specifically for that purpose, but because no other federal program fills the gap that Medicare's custodial care exclusion leaves.

The practical consequence is that most Americans who need extended nursing home or home-based long-term care and cannot afford it privately end up on Medicaid — after spending down their assets to the eligibility threshold. This is not a failure of planning in every case; for people without substantial assets, Medicaid may be the appropriate and expected funding path. For people with retirement assets they hoped to preserve, arriving at Medicaid through asset depletion represents a planning gap.

The Two Qualification Thresholds: Financial and Clinical

Medicaid eligibility for long-term care is not simply a matter of having low assets. Two entirely separate thresholds must both be met — and meeting one does not guarantee meeting the other.

The financial threshold is the more widely understood requirement. For a single person in most states, countable assets must generally be at or below approximately $2,000. Income rules vary by state — some states require income to fall below a cap (income-cap states); others allow spend-down of excess income through incurred medical expenses (medically needy states). For married couples, federal spousal protection rules create a more complex structure.

The clinical threshold is equally important and less often discussed. Medicaid also requires that the applicant meet the state's level-of-care criteria — meaning a clinical assessment must confirm that the person requires nursing facility-level care or, for HCBS waivers, the applicable home-based care level. A person with significant assets could not simply spend down and apply for Medicaid's long-term care benefit if they do not also meet clinical criteria. Conversely, a person with very limited assets may be financially eligible but not yet meet the clinical threshold.

BOTH THRESHOLDS MUST BE MET

Financial eligibility alone does not trigger Medicaid long-term care coverage. The applicant must also be assessed as meeting the clinical level-of-care standard for the type of Medicaid coverage sought. This assessment is typically conducted by the state Medicaid agency or a designated assessor. The clinical standard for nursing facility Medicaid generally corresponds to a significant number of ADL dependencies; HCBS waiver standards vary by state and program.

Countable vs. Exempt Assets

Medicaid does not count all assets equally. The eligibility determination separates assets into two categories: countable (which must generally be spent down to the eligibility threshold) and exempt (which are not counted and do not need to be depleted).

Understanding this distinction is essential because the common belief — "I have to lose everything before Medicaid kicks in" — is partially inaccurate. Some assets are protected by design. The primary residence, for example, is exempt during the recipient's lifetime under certain conditions. However, "exempt" does not mean permanently protected.

THE HOME EXEMPTION AND ESTATE RECOVERY

The primary residence is exempt from Medicaid's asset count while the recipient or their spouse is living there. However, federal law requires states to seek recovery from the estate for Medicaid long-term care costs paid for individuals age 55 and older — after the death of the recipient and any surviving spouse. The scope of recovery varies by state: some states recover only from probate assets; others pursue expanded recovery from jointly held assets, living trusts, and transfer-on-death accounts."Exempt during life" and "protected from recovery" are not the same thing.

Medicaid's Role in the Long-Term Care System

Despite its means-tested structure, Medicaid is the dominant payer in the long-term care system by a wide margin. Approximately 62% of nursing home residents nationally receive Medicaid coverage. This reflects a structural reality: most people who need extended nursing facility care eventually deplete their assets and qualify for Medicaid, regardless of their asset position at the start of the care episode.

This dynamic has important implications:

-

For people with modest assets, Medicaid may be the expected and planned-for outcome from the beginning — a legitimate safety net operating as intended

-

For people with substantial retirement assets, Medicaid represents the end of a spend-down process that may have consumed most of what they accumulated

-

For families engaged in deliberate legal planning, Medicaid may be structured as a component of a broader long-term care plan — with assets protected through legal instruments and the look-back period observed in advance

Medicaid functions differently at different asset levels. Its role as a safety net, a planning tool, and a system of last resort all apply to different segments of the population facing long-term care needs.

HCBS Waivers: Medicaid's Home-Based Care Pathway

Medicaid's primary long-term care benefit — the institutional benefit — funds nursing facility care. A separate and distinct pathway, Home and Community Based Services (HCBS) waivers, allows states to use Medicaid funding for home-based and community-based care as an alternative to nursing facility placement.

HCBS waivers are significant for several reasons:

-

They can fund personal care aides, adult day services, home modifications, and other support services that allow people to remain at home or in a community setting rather than a nursing facility

-

They are operated at the state level under federal waiver authority, meaning eligibility criteria, covered services, and availability vary significantly by state

-

Most states have wait lists for HCBS waiver programs — availability is not guaranteed and may not align with when care is actually needed

-

Eligibility typically requires meeting the same level-of-care criteria as nursing facility Medicaid, though some states have intermediate standards

The HCBS waiver pathway is one reason that "Medicaid only covers nursing homes" is inaccurate. Medicaid can fund home-based care — but only through these waiver programs, which are subject to state-specific rules and availability constraints that do not exist for the institutional benefit.

What Medicaid Does Not Cover

Medicaid's long-term care coverage, while substantial, is not unlimited. Several care settings and costs fall outside

Medicaid coverage even for eligible individuals:

-

Room and board: Assisted living in most states

-

Medicaid does not cover assisted living room and board in most states. Some states have limited Medicaid funding for personal care services within assisted living, but full room and board coverage comparable to nursing facility coverage is not available in the majority of states.

-

Private room upgrades: Private-pay amenities in nursing facilities

-

Medicaid pays at the Medicaid rate for semi-private room accommodation. A private room requires a private-pay supplement or a facility willing to accept Medicaid for private rooms.

-

Facility choice: Non-Medicaid-certified facilities

-

Medicaid only pays for care in facilities that accept Medicaid reimbursement. Many higher-end facilities do not participate in Medicaid, or limit the number of Medicaid beds. A person relying on Medicaid may not be able to remain in their current facility if it does not have Medicaid capacity.

-

Level-of-care limits: Care above the approved level of care

-

Medicaid funds care at the clinically assessed level. Services above that level require supplemental private funding.

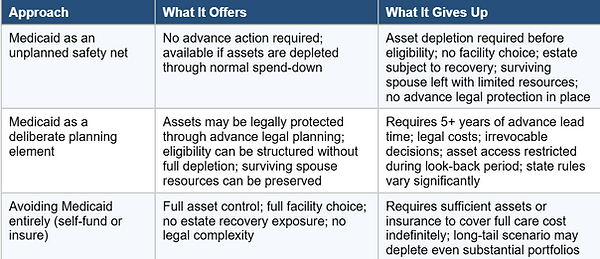

The Trade-Off: Medicaid as Safety Net vs. Medicaid as Plan

The role Medicaid plays in a long-term care situation depends largely on whether it arrives as the result of deliberate planning or as a default outcome of asset depletion. These are meaningfully different scenarios with different consequences.

Neither the safety-net path nor the deliberate planning path is universally correct. The right approach depends on the individual's asset level, health, age, family structure, and values around asset preservation. The point of naming the trade-off explicitly is that arriving at Medicaid through unplanned asset depletion and arriving through deliberate legal planning are not the same outcome — even if both result in Medicaid eligibility.

Why Medicaid Is an Emotionally Charged Subject

EMOTIONAL ACKNOWLEDGMENT

Many people associate Medicaid with poverty and carry a strong aversion to the idea of "being on Medicaid." For people who have worked and saved throughout their lives, the prospect of spending down to $2,000 in assets before a program kicks in feels like a fundamental injustice. That response is understandable. The spend-down requirement is real and significant. What this page offers is not reassurance — it is clarity about what Medicaid is, how it actually works, and what options exist for those who want to plan around it. Medicaid can be approached with knowledge or encountered as a surprise. This page is for the former.

Summary

Medicaid is a means-tested federal-state public assistance program — not an earned benefit like Medicare. It is the primary payer for long-term custodial care in the United States, covering approximately 62% of nursing home residents nationally.

Eligibility requires meeting two separate thresholds: financial (assets generally at or below $2,000 for a single person in most states) and clinical (meeting the state's level-of-care standard for the type of care sought). Both must be satisfied.

Countable assets must be spent down to the eligibility threshold; exempt assets — including the primary residence under certain conditions — are not counted. However, the home exemption does not prevent estate recovery after death. Federal law requires states to recover Medicaid long-term care costs from the estates of recipients age 55 and older.

Medicaid can function as an unplanned safety net, as a deliberate planning element, or as the unavoidable outcome of a long care episode that depletes assets. Understanding what it is and how it works is the prerequisite for any conversation about the role it should — or should not — play in a long-term care plan.

Frequently Asked Questions

What is the difference between Medicare and Medicaid?

Medicare is a federal health insurance program for people 65 and older, funded by payroll taxes, and available regardless of income or assets. It covers acute medical care, hospitalization, physician services, and short-term skilled rehabilitation. It does not cover ongoing custodial care. Medicaid is a joint federal-state public assistance program, means-tested, available only to people whose assets and income fall below defined thresholds. It is the primary payer for long-term custodial care in the U.S. The programs were created together in 1965 but serve different populations and cover different services.

Does Medicaid pay for nursing home care?

Yes — Medicaid is the primary payer for nursing home care in the United States, covering approximately 62% of nursing home residents nationally. To qualify, a person must meet both the financial eligibility threshold (assets generally at or below ~$2,000 for a single person in most states) and the clinical level-of-care standard assessed by the state Medicaid agency. Medicaid pays the facility at the Medicaid rate, which is typically lower than private-pay rates. The recipient must apply substantially all of their income toward the cost of care, retaining only a small personal needs allowance.

How much money can you have and still qualify for Medicaid for nursing home care?

In most states, a single person must have $2,000 or less in countable assets to qualify for Medicaid long-term care coverage. Some states have slightly higher thresholds; rules vary. For married couples, the community spouse (the one not in a facility) is protected by the Community Spouse Resource Allowance (CSRA), which in 2026 allows the community spouse to retain up to $162,660 in countable assets. Income rules also apply and vary by state — some states require income below a cap; others allow excess income to be spent on medical expenses. These are 2026 federal figures; state-specific limits should be verified.

Does Medicaid cover assisted living?

Generally, no — Medicaid does not cover room and board in assisted living facilities in most states. Some states have limited Medicaid funding for personal care services provided within an assisted living setting, but this coverage is typically partial and limited in availability. Assisted living residents on Medicaid in states with such programs may have their personal care services covered while still being responsible for the facility's room and board cost. Full Medicaid coverage comparable to nursing facility coverage is not available for assisted living in the majority of states. HCBS waiver programs can sometimes fund supportive services in assisted living-type settings, subject to state rules and wait lists.

What is a Medicaid spend-down?

A Medicaid spend-down refers to the process of depleting countable assets to the eligibility threshold — typically $2,000 for a single person — before Medicaid will begin covering long-term care costs. Assets must generally be spent on legitimate personal expenses or care costs. Transferring assets for less than fair market value — giving money to family members, for example — is examined under the 60-month look-back rule and may result in a penalty period during which Medicaid will not pay for care. The spend-down process is addressed in detail in following articles.

What is an HCBS waiver?

HCBS stands for Home and Community Based Services. HCBS waivers are state-operated Medicaid programs that fund care provided in home and community settings — such as personal care aides, adult day services, and supportive services — as an alternative to nursing facility placement. They require federal approval and operate under specific eligibility criteria and covered services defined at the state level. Availability varies significantly: most states have wait lists for HCBS waiver programs, and the services and funding levels differ widely. HCBS waivers allow Medicaid to fund home-based care, but they are not universally available or guaranteed.

Does Medicaid take your house?

Medicaid does not take your house while you are alive and living in it (or while a spouse lives there). The primary residence is an exempt asset for Medicaid eligibility purposes. However, federal law requires states to seek recovery of Medicaid long-term care costs from the estates of recipients age 55 and older, after the death of both the recipient and any surviving spouse. This means the home — which was exempt during the recipient's life — may be subject to a Medicaid estate recovery claim after death. The scope of recovery varies by state: some states limit recovery to probate assets; others pursue expanded recovery from jointly held property, living trusts, and transfer-on-death accounts. "The home is exempt" and "the home is permanently protected" are not the same statement.

Can I give my money to my children so I qualify for Medicaid?

Transferring assets to family members for less than fair market value within the 60-month (five-year) period before a Medicaid application will generally result in a penalty period during which Medicaid will not pay for care. The penalty is calculated by dividing the value of the disqualifying transfer by the state's average monthly nursing home cost — the result is the number of months Medicaid will not pay. This rule applies regardless of the reason for the transfer or the recipient's intent. Gifts made more than five years before the application date are generally outside the look-back window.

Is Medicaid the same as welfare?

Medicaid is a means-tested public assistance program funded by federal and state governments — in that structural sense, it is categorized alongside other public assistance programs. The term "welfare" carries associations that many people find stigmatizing, and whether Medicaid for long-term care is framed that way varies significantly. For the purposes of financial planning, what matters is the program's structure: it requires asset depletion to a low threshold, imposes an income contribution requirement, restricts facility choice to Medicaid-accepting providers, and subjects the estate to recovery after death. These are the material features of the program that affect planning decisions.

What is the income limit for Medicaid long-term care?

Medicaid income rules for long-term care vary by state. Income-cap states (sometimes called 300% states) require that the applicant's income be below a defined cap — typically 300% of the federal Supplemental Security Income (SSI) benefit level. In 2026 this threshold is approximately $2,829/month. Applicants with income above the cap in these states must use a Qualified Income Trust (also called a Miller Trust) to become eligible. Medically needy states allow applicants with higher income to spend down excess income on medical expenses until they reach the state's medically needy threshold. Income that qualifies is then generally applied to the cost of care, with the recipient retaining only a small personal needs allowance (typically $30–$130/month depending on the state).

This page does not advise on Medicaid planning strategies, asset protection structures, or the advisability of Medicaid for any individual. Medicaid rules are highly state-specific — the figures cited here are federal standards and 2026 federal thresholds; state rules vary and should be verified with a licensed elder law attorney in the relevant state.

This page is part of the Wealth Solutions Network Reference Library, a first-principles financial education resource. It explains — it does not advise.